Monthly Cotton Economic Letter (2018.6)

Jul 20, 2018 | by

Recent price movement

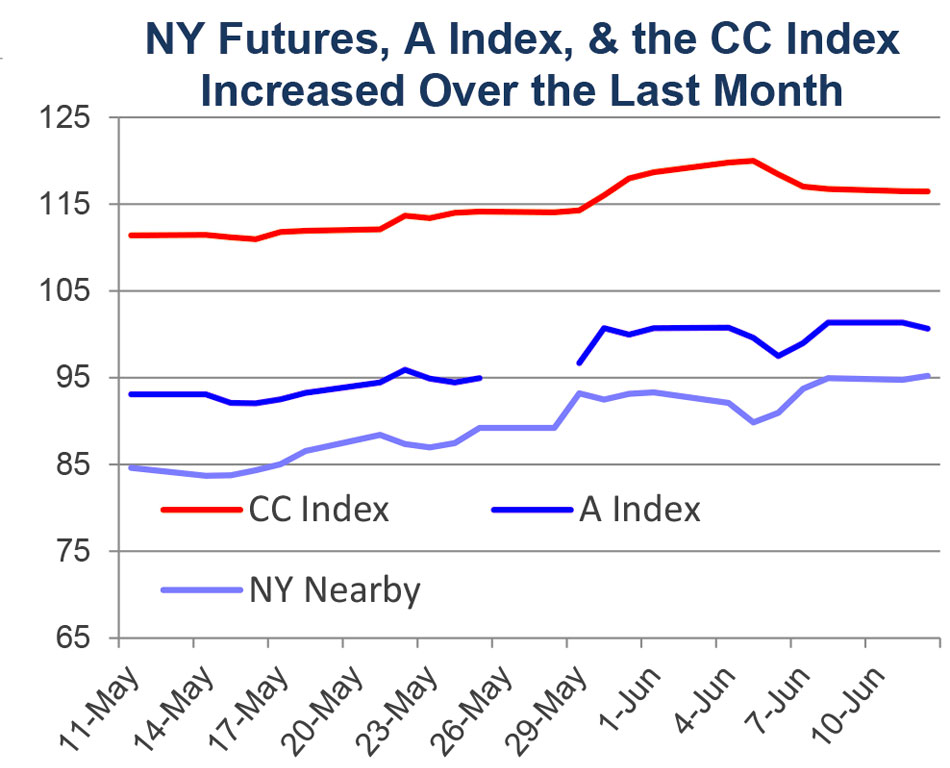

The global cotton market was volatile over the past month, with values for most benchmark prices moving strongly higher in the second half of May.

l Values for the July NY futures contract surged from levels near 84 cents/lb a month ago to those near 95 cents/lb recently (+13%). Values for the December NY futures contract rose more sharply than those for July (from 80 cents/lb in early May to 93 cents/lb, or +19%) , narrowing the discount for 2018/19 prices (December futures) relative to 2017/18 prices (July futures).

l The A Index climbed alongside NY futures. One month ago, values for the A Index were near 94 cents/lb. The latest values have been over 100 cents/lb, marking the first time since March 2012 that the A Index has been over a dollar.

l Chinese cotton futures (ZCE) were also volatile. The most actively traded January contract increased 15% between mid-May and the end of the month (from 16,400 to 18,900 RMB/ton). More recently, Chinese futures have declined, with the latest values near 17,700 RMB/ton. Contrary to NY futures, the forward curve (graph comparing prices for futures contracts that expire in the near-term relative to those that expire further into the future) for Chinese futures is upward sloping.

l Chinese spot prices, as represented by the Chinese Cotton (CC) Index (3128B grade), increased in both domestic and international terms (from 111 to 117 cents/lb or from 15,500 to 16,500 RMB/ton).

l Indian spot prices for the Shankar-6 quality increased from 79 to 87 cents/lb or from 42,000 to 45,900 INR/candy.

l Pakistani spot prices were comparatively stable over the past month, trading between 77 and 80 cents/lb or 7,400 and 7,500 PKR/maund.

Supply, demand, & trade

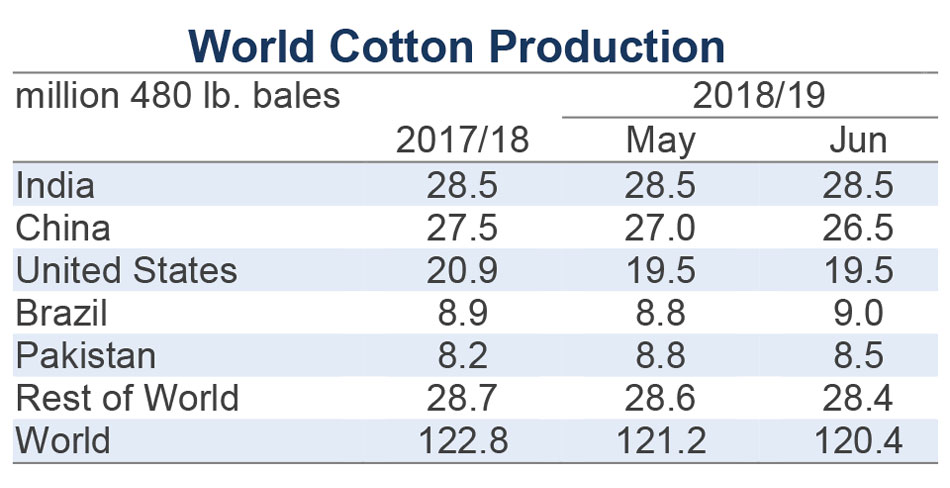

This month’s USDA report featured a reduction to the forecast for 2018/19 global production (-790,000, from 121.2 to 120.4 million bales) and a marginal change to the global mill-use forecast (-85,000, holding at 125.4 million bales). With the estimate for 2018/19 beginning stocks unchanged, the net effect of this month’s revisions was to lower the forecast for 2018/19 ending stocks by virtually the same amount as the reduction in the production number (-725,000, from 83.7 to 83.0 million).

At the country-level, the largest changes to 2018/19 harvest expectations were for China (-500,000 bales, from 27.0 to 26.5 million), Pakistan (-300,000, from 8.8 to 8.5 million), Australia (-200,000, from 4.0 to 3.8 million), and Brazil (+200,000, from 8.8 to 9.0 million). Despite continued hot and dry conditions in the important West Texan region, no change was made to the 2018/19 U.S. production forecast.

For mill-use, the largest country-level revisions to 2018/19 forecasts were for South Korea (-225,000, from 1.0 to 0.8 million bales), Uzbekistan (+100,000, from 2.7 to 2.8 million), and Vietnam (+100,000, from 7.4 to 7.5 million).

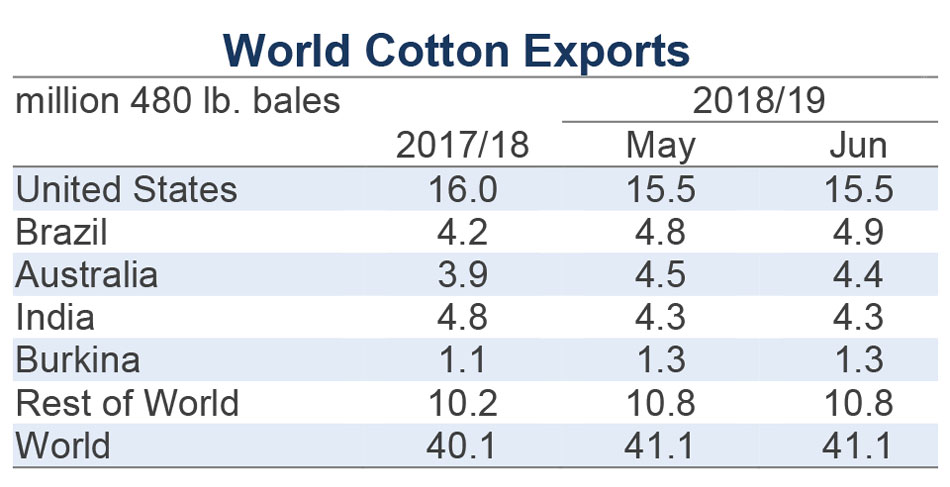

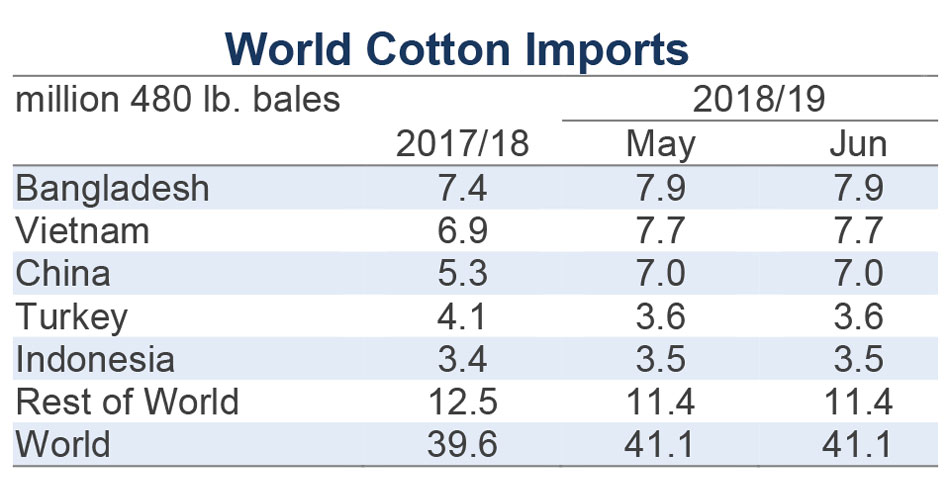

In terms of trade, the global 2018/19 projection was nearly unchanged (-65,000, from 41.1 to 41.0 million bales), while the estimate for 2017/18 increased 420,000 bales (from 39.7 to 40.1 million).

For imports, the only notable revisions to 2018/19 projections were for South Korea (-225,000, from 1.0 to 0.8 million) and Pakistan (+100,000, from 2.1 to 2.2 million). For 2017/18 import figures, the largest changes were for China (+200,000 bales, from 5.1 to 5.3 million), India (+100,000, from 1.7 to 1.8 million), and South Korea (-125,000, from 1.0 to 0.9 million).

For exports, notable revisions to 2018/19 projections were for Australia (-100,000, from 4.5 to 4.4 million) and Brazil (+100,000, from 4.8 to 4.9 million). For 2017/18 export figures, the largest changes were for Uzbekistan (-200,000, from 1.3 to 1.1 million), Kazakhstan (+140,000, from 140,000 to 280,000), India (+250,000, from 4.5 to 4.8 million), and the U.S. (+500,000, from 15.5 to 16.0 million).

Price outlook

The pattern of movement suggests that the latest round of global volatility originated in China. In response to domestic volatility, the Chinese government made a series of announcements in early June. Generally, these statements emphasized the existence of adequate supply in the near-term and the ability to secure additional cotton as needed into the future. Specific comments indicated that reserve volumes are sufficient, and that the current round of sales can be extended an additional month (initially scheduled from March through the end of August, but can continue through the end of the September as has been done the past two years). To curb speculation in cotton sold from reserves, the government banned traders/merchants from buying at auction (only spinning mills can buy, and mills are prohibited from reselling).

Beyond currently warehoused supplies, Chinese officials indicated that adverse weather throughout the spring in the important Xinjiang province (home to 75-80% of Chinese production) should have only a limited effect on yield, and that fears of a collapse in the domestic harvest were overblown. Importantly for the rest of the world, the Chinese government also reported that plans are in place to increase import quota, with officials indicating that sliding-scale quota can be released in the near future.

These comments highlight a central source of uncertainty for the global cotton market during the 2018/19 crop year, which is how much more China cotton may import. With dry conditions affecting the largest growing region of the largest exporting country (West Texas, U.S.), the possibility of stronger than forecast Chinese imports underline the possibility of lower than expected ending stocks outside of China. Current USDA forecasts suggest that ending stocks outside of China will increase in 2018/19, adding to the record volume estimated for 2017/18. This volume will serve as a buffer against rising Chinese import demand, but there are questions about the accuracy of the USDA’s estimate for non-Chinese stocks (e.g., wide separation between USDA’s number for Indian stocks relative to domestic estimates). The actual volume of stocks available for export to China, as well as the size of the increase in Chinese imports can be expected to determine price levels in 2018/19 and beyond.