Monthly Cotton Economic Letter (2018.5)

Jun 20, 2018 | by

Recent price movement

NY futures experienced volatility recently, with the net effect being a slight increase in prices. The A Index also moved slightly higher, while other benchmark prices were stable.

l NY futures moved higher in early May, but retreated in the latest trading. July futures, reflective of 2017/18 supplies, briefly broke above 85 cents/lb, but have since returned to levels near 84 cents/lb December futures, representative of expectations following the onset of the 2018/19 harvest, briefly climbed as high as 81 cents/lb, but have since returned to levels below 80 cents/lb.

l The A Index moved higher alongside NY futures, but the magnitude of change was smaller. Current values for the A Index are 94 cents/lb, one month ago, they were 92 cents/lb.

l Chinese cotton prices, as represented by the Chinese Cotton (CC) Index (3128B grade) were stable in both domestic (near 15,500 RMB/ton) and international terms (near 111 cents/lb).

l Indian spot prices for the Shankar-6 quality moved slightly higher in domestic terms (from 41,000 to 42,000 INR/candy), but were virtually unchanged in international terms (near 80 cents/lb) over the past month.

l Pakistani spot prices were steady in both domestic (7,500 PKR/maund) and international terms (near 80 cents/lb).

Supply, demand, & trade

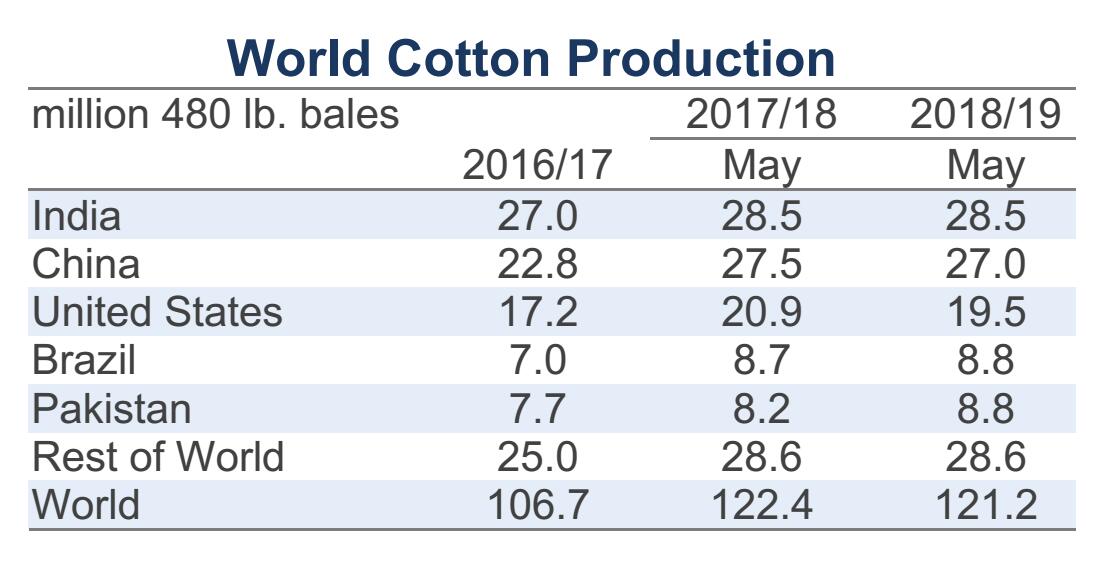

In May, the USDA releases its first complete set of forecasts for an upcoming crop year. Projections suggest world production in 2018/19 will be 121.2 million bales, a marginal decrease relative to the 122.4 million bales grown in 2017/18. Global mill-use is expected to increase 4% (from 120.7 million bales in 2017/18) and reach 125.4 million bales in 2018/19. If realized, this would be the highest level of consumption ever (current record of 124.2 million was set in 2006/07).

With the forecast for world production below the forecast for mill-use, world ending stocks are projected to decrease (-4.5 million bales, from 88.2 to 83.7 million). The global decline is expected to be driven by China, where stocks are predicted to drop 7.6 million bales (from 41.0 to 33.4 million). For the collection of countries outside of China, ending stocks are forecast to increase 3.1 million bales (from 47.2 to 50.3) and are expected to set a new record (current record is the figure for 2017/18).

The forecast for a smaller world harvest in 2018/19 is primarily a result of expectations of smaller harvests from the U.S. (-1.4 million bales, from 20.9 to 19.5 million), Australia (-800,000, from 4.8 to 4.0 million), and China (-500,000, from 27.5 to 27.0 million). Partially offsetting these declines are projected increases for Pakistan (+600,000 bales, from 8.2 to 8.8 million) and Turkey (+300,000, from 4.0 to 4.3 million). Indian production is projected to be unchanged at 28.5 million bales.

The global increase in mill-use is expected to result from growth across a broad range of countries. The largest gains are expected in China (+1.5 million bales, from 40.0 to 41.5 million), India (+1.0 million, from 24.2 to 25.2 million), Vietnam (+800,000, from 6.6 to 7.4 million), Bangladesh (+500,000, from 7.3 to 7.8 million), Uzbekistan (+300,000, from 2.4 to 2.7 million), and Turkey (+200,000, from 7.2 to 7.4 million).

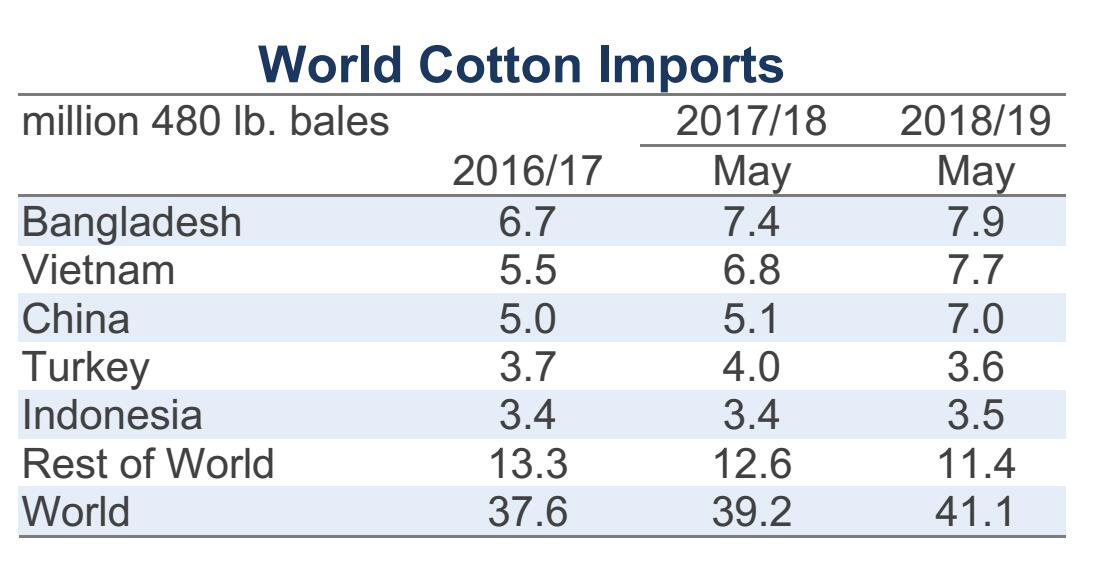

Global cotton trade is forecast to rise from 39.2 in 2017/18 to 41.1 million bales in 2018/19. The largest year-over-year changes to imports are forecast for China (+1.9 million bales, from 5.1 to 7.0 million), Vietnam (+1.1 million, from 6.8 to 7.7 million), and Bangladesh (+500,000, from 7.4 to 7.9 million). With bigger domestic harvests, decreases are expected in Pakistan (-800,000 bales, from 2.9 to 2.1 million) and Turkey (-350,000, from 4.0 to 3.6 million).

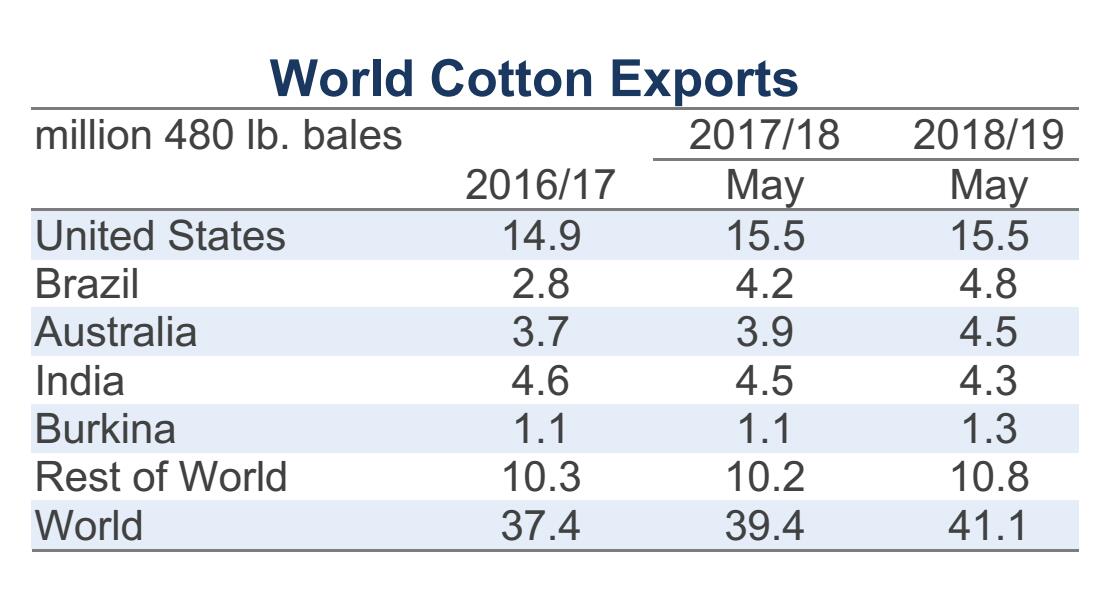

The largest year-over-year changes to exports in 2018/19 are forecast for Australia (+600,000, from 3.9 to 4.5 million), Brazil (+600,000, from 4.2 to 4.8 million), and the African Franc Zone (+400,000 bales, from 4.1 to 4.4 million). Decreases are projected for Uzbekistan (-300,000 bales, from 1.3 to 1.0 million) and India (-200,000, from 4.5 to 4.3 million). A notable month-over-month change to estimates for the 2017/18 crop year included the 500,000 bale addition to the U.S. export forecast (to 15.5 million, which ranks as the second highest on record). In 2018/19, U.S. exports are forecast to reach the same level.

Price outlook

Examination of world supply and demand figures in recent decades suggests that it is possible to delineate multi-year periods by their dominant fundamental factors. For example, the period leading up to the price spike (2006/07-2009/10) can be characterized by falling global acreage and production paired with the effects of the global financial crisis on mill-use. After the spike (2011/12-2014/15), the global cotton market could be characterized by the Chinese policies of the time, with strong Chinese import demand supporting world cotton prices, acreage, and production while also inhibiting global consumption growth. The current multi-year period (2015/16-2017/18) could be defined by low Chinese imports, rising global acreage and production (supported by lower prices for competing crops like corn and soybeans), as well as accelerating growth in global mill-use.

2018/19 could prove to be a year of transition into a new multi-year period defined by a new set of defining market fundamental conditions. One change in fundamentals could come from production. After a couple of years of strong growth, global production is expected to be flat to lower in 2018/19. This is primarily a result of challenges facing the world’s largest producing countries (e.g., repeated pest attacks in India, rising production costs in China, and recurring weather-related issues in the U.S. and Australia). Given these challenges, the curve in the upward trajectory in production expected in 2018/19 could signal the onset of a sideways trend in world cotton production.

Another major shift in market fundamentals will likely come from increased Chinese imports. Many forecasting organizations are projecting only a slight increase this crop year (USDA +1.9 million bales, Cotlook +2.3 million, ICAC +1.6 million), but China’s persistent production/consumption deficit of 12-15 million bales, along with the on-going drawdown of China’s reserve stocks, suggest that China will need to increase its imports more dramatically at some point in the relatively near future.

When that happens, higher Chinese import demand should pull stocks held outside of China lower. There are lingering questions regarding stock levels in certain countries outside of China (notably India), but the direction of change for the collective volume in storage outside of China has been one of increase in recent years. Those increases will serve as a buffer against rising Chinese import demand, but with on-going production-related questions facing several exporters (India, U.S., and Australia) an eventual reduction in world-less-China stocks could be expected. This suggests eventual upward pressure on cotton prices. The extent to which any of this happens will depend on the details concerning the timing and volume of changes in Chinese imports, how global production responds, and what the weather may bring.