Monthly Cotton Economic Letter (2018.4)

May 10, 2018 | by

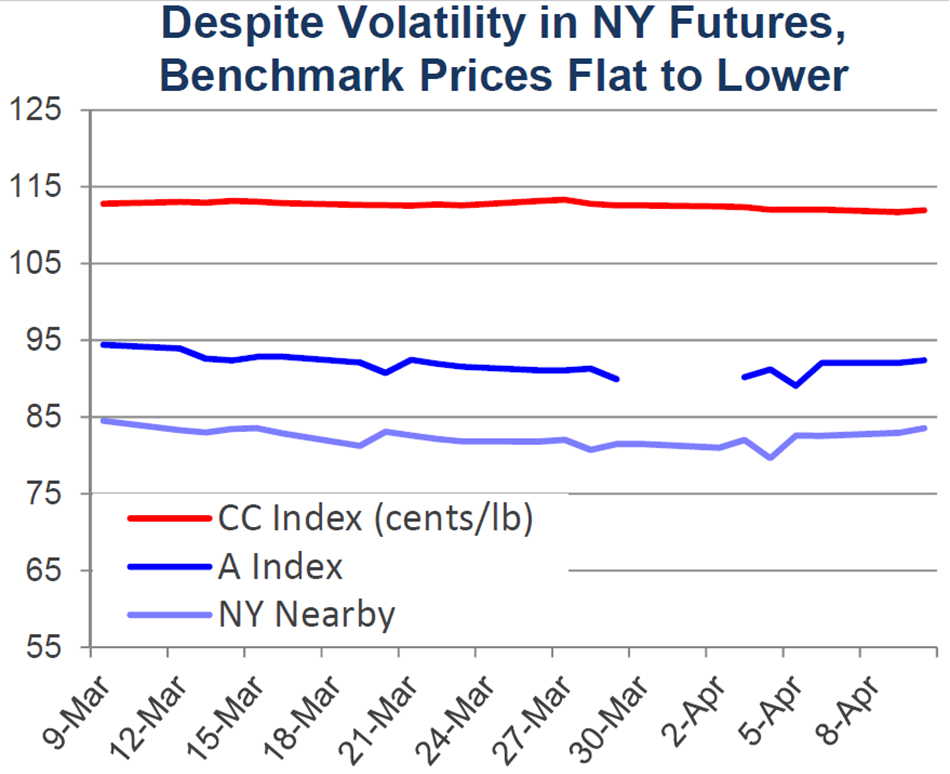

Recent price movement

NY futures experienced volatility in early April. Current values for all benchmark prices are flat to lower relative to levels one month ago.

l With the announcement that cotton was listed among the U.S. products that China could hit with an increase in tariffs, NY futures declined sharply on April 4th. In trading that soon followed, prices completely recovered and have since been relatively stable. The latest values for the May and July contracts have been holding near 83 cents/lb while December futures have been holding near 78 cents/lb.

l The A Index was generally stable over the past month, trading between 90 and 93 cents/lb.

l In international terms, the China Cotton Index (CC Index, 3128B) decreased marginally, from 113 to 112 cents/lb. In domestic terms, the CC Index also decreased slightly, from 15,700 RMB/ton to 15,500 RMB/ton.

l Prices for the Indian Shankar-6 quality were also generally stable. Remaining near 80 cents/lb in international terms and near 40,800 INR/candy in domestic terms.

l Pakistani spot prices increased in mid-March, climbing from 78 cents/lb early in the month to 84 cents/lb. Since then, prices have decreased to levels near 77 cents/lb. In domestic terms, values rose from 7,100 PKR/maund to 7,600 PKR/maund before retreating to 7,300 PKR/maund.

Supply, demand, & trade

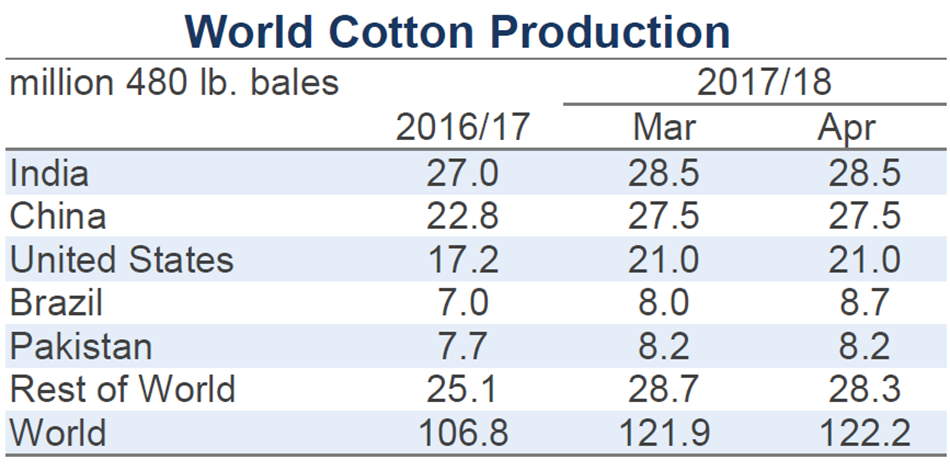

This month’s USDA report featured a slight increase to global production (+245,000 bales, from 121.9 to 122.2 million) and a slight decrease to global mill-use (-405,000 bales, from 120.8 to 120.4 million) figures for 2017/18. A series of revisions to historical estimates for Australia, Brazil, and Uzbekistan had a net effect of lowering 2017/18 global beginning stocks by 900,000 bales (from 87.7 to 86.8 million). In combination, all of this month’s changes pulled the forecast for 2017/18 global ending stocks slightly lower (-555,000 bales, from 88.9 to 88.3 million).

At the country-level, the largest updates to production estimates included a 700,000 bale addition for Brazil (from 8.0 to 8.7 million) and a 425,000 bale reduction for Sudan (from 900,000 to 475,000). For mill-use, notable changes were for Vietnam (+100,000, from 6.5 to 6.6 million), Indonesia (-100,000, from 3.5 to 3.4 million), and India (-300,000, from 24.5 to 24.2 million).

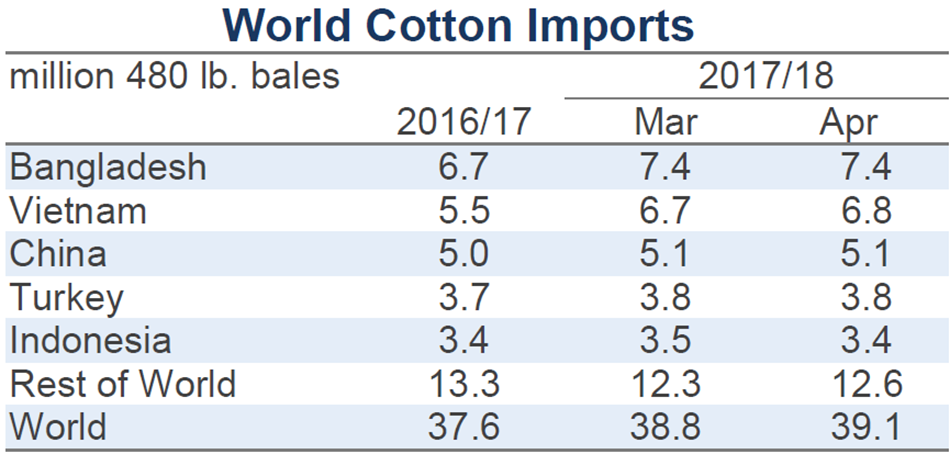

Global trade estimates increased slightly (+225,000 bales, from 38.8 to 39.1 million). The largest changes to import figures included those for Pakistan (+200,000, from 2.7 to 2.9 million), Mexico (+100,000, from 0.9 to 1.0 million), Vietnam (+100,000, from 6.7 to 6.8 million), and Indonesia (-100,000 from 3.5 to 3.4 million). The largest changes to export figures included those for India (+300,000, from 4.2 to 4.5 million), the U.S. (+200,000 bales, from 14.8 to 15.0 million), and Uzbekistan (+100,000, from 1.1 to 1.2 million), Australia (-200,000, from 4.4 to 4.2), and Sudan (-150,000, from 500,000 to 350,000).

Price outlook

The stream of trade-related announcements flowing from the U.S. and China adds another layer of uncertainty to the cotton market. In a release on April 3rd, the U.S. did not include any apparel or textile items on the list of Chinese goods (collectively valued at $50 billion) that could be hit with increased tariffs. On April 4th, China included cotton on the list of U.S. goods (collectively valued at $50 billion) that it could hit with higher tariffs. The following day, the U.S. indicated that it is researching an even larger list of additional goods (collectively valued at $100 billion) from China that could also face higher tariffs. The items on the second U.S. list have yet to be released.

Little is known about future implementation of any of these announcements. Negotiations should take place over the next several months and will determine whether or not any of the proposed tariff increases will actually be enforced. If the proposals are enforced, they will influence trade patterns.

One outcome that could be expected is that U.S. exports to China would decrease because with the additional 25% duty U.S. cotton would become more expensive relative to other origins. However, the size of the decrease would be smaller than if the tariffs were imposed several years ago. A reason for this is that China sharply reduced its imports from all origins in recent years as it encouraged the mill-use of government-controlled reserve stocks over imports. As a result, U.S. exports to China in the past two crop years have been 0.9 and 2.3 million bales, much lower than the longer-term average over four million bales. With U.S. exports to China already lower, there is simply less room to fall than there would have been several years ago.

While U.S. sales to China decreased, the U.S. increased sales to other markets, notably to Vietnam and South Asia. Despite lower exports to China, the U.S. shipped the second highest overall volume of cotton on record last crop year. The share that went to China in 2016/17 was 15% (far lower than the proportions between 30% and 60% that were common in the 2000s), which implies that 85% of U.S. exports went elsewhere. The large percentage going to other markets also implies that the U.S. has less exposure to a downturn in Chinese demand than five to ten years ago.

Nonetheless, the importance of China as a customer of U.S. and global cotton exporters should not be understated. Given the drawdown in reserve stocks over the past several years, China is approaching the transition point when it should begin to import significantly more cotton. The prospect of China eventually returning to import volumes between 10-15 million bales should be encouraging for cotton exporters all over the world.

If the proposed tariffs are implemented alongside increases in Chinese imports, it would affect the volume of U.S. cotton that could go to China. However, no other country has an exportable surplus rivaling that from the U.S. As a result, if China pulls in more cotton from other exporters, it could be expected that the corresponding tightness of non-U.S. exportable supply would push higher U.S. exports into import markets outside of China.