Prosperity of professional market declines sharply from January to February

Mar 09, 2020 | by

The monitoring results of the China Commercial Circulation Association of Textile and Apparel (CATA) show that from January to February 2020, the national textile and apparel professional market manager’s prosperity index was 16.13, down 33.82 percentage points from 49.95 in December; the professional market merchants’ prosperity index was 36.40, down 14.06 percentage points from 50.46 in December.

1. The manager’s and merchants’ prosperity index decline

Data show that from January to February, the national textile and apparel professional market manager’s prosperity index and the professional market merchants’ prosperity index experienced a large decline.

1.1 Managers’ prosperity index decreased by 33.82 percentage points

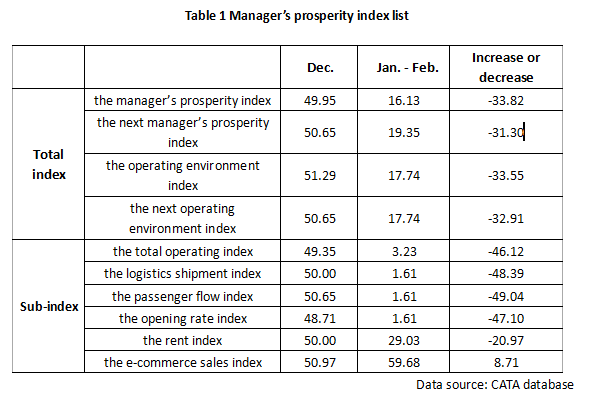

From the perspective of manager’s prosperity index, among the total index, the manager’s prosperity index of January to February was 16.13, down 33.82 percentage points from 49.95 in December; the operating environment index was 17.74, down 33.55 percentage points from 51.29 in December.

In the sub-index, the total operating index was 3.23, down 46.12 percentage points from 49.35 in December; the logistics shipments index was 1.61, down 48.39 percentage points from 50.00 in December; the passenger flow index was 1.61, down 49.04 percentage points from 50.65 in December; the opening rate index was 1.61, down 47.10 percentage points from 48.71 in December; the rent index was 29.03, down 20.97 percentage points from 50.00 in December; the e-commerce sales index was 59.68, up 8.71 percentage points from 50.97 in December.

1.2 Merchants’ prosperity index decreased by 14.06 percentage points

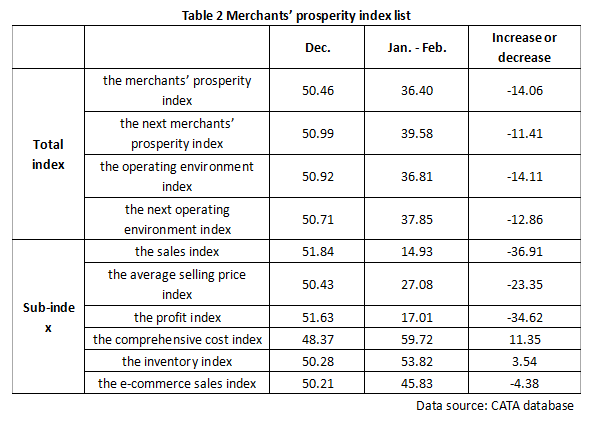

From the perspective of the merchants’ climate index, among the total index, the merchants’ climate index was 36.40, down 14.06 percentage points from 50.46 in December; the operating environment index was 36.81, down 14.11 percentage points from 50.92 in December.

In the sub-index, the sales index was 14.93, down 36.91 percentage points from 51.84 in December; the average selling price index was 27.08, down 23.35 percentage points from 50.43 in December; the profit index was 17.01, down 34.62 percentage points from 51.63 in December; the comprehensive cost index was 59.72, up 11.35 percentage point from 48.37 in December; the inventory index was 53.82, up 3.54 percentage points from 50.28 in December; the e-commerce sales index was 45.83, down 4.38 percentage points from 50.21 in December.

2. Data analysis

2.1 Affected by the Spring Festival holiday and the epidemic, market indexes fell sharply.

In January - February, the proportion of selected total market operations decreased by 93.55%, up 74.20 percentage points from 19.35% in December; the proportion of selected market logistics shipments decreased by 96.77%, up 77.42 percentage points from 19.35% in December; the proportion of selected passenger flow decreased by 96.77%, up 83.87 percentage points from 12.90% in December. From January to February, the textile and apparel professional markets across the country were affected by factors such as the Spring Festival holiday and the COVID-19, which delayed the opening time. The market’s total business operations, logistics shipments, and passenger flow all fell sharply, and the professional market operations basically stopped.

2.2 Professional markets try to mitigate the impact of the epidemic through online sales

From January to February, the proportion of increase in e-commerce sales in selected markets was 35.48%, up 19.35 percentage points from 16.13% in December; the proportion of increase in e-commerce sales in selected merchants was 18.06%, up 10.97 percentage points from 7.09% in December. In case of failure to operate normally, the proportion of e-commerce sales in the textile and apparel professional market and merchants increased. The manager’s e-commerce sales index was 59.68, up 8.71 percentage points from 50.97 in December, and it was the only index among all managers’ indexes that exceeded the 50 threshold. After nearly two months of operation shock caused by the COVID-19 epidemic, China’s textile and apparel professional market may pay more attention to the exploration of online sales models in the future, increase investment, and accelerate the transformation of online and offline integration and development.

2.3 Merchants’ comprehensive cost index and inventory index rose

The comprehensive cost index was 59.72, up 11.35 percentage points from 48.37 in December; the inventory index was 53.82, up 3.54 percentage points from 50.28 in December. From January to February, the merchants who could not carry out daily operations at the market stalls mostly chose to sell some products through online channels, and the inventory pressure was slightly eased; meanwhile, expenses were saved in terms of labor, publicity, miscellaneous expenses etc. The cost pressure is relatively small.

2.4 The overall merchants’ prosperity index is higher than the manager’s prosperity index

From January to February, the merchants’ prosperity index was 36.40, and the manager’s prosperity index was 16.13; the merchants’ operating environment index was 36.81, and the manager’s operating environment index was 17.74. When the professional market ceased to operate, merchants still achieved a certain amount of merchandise sales through online sales and other channels. The overall prosperity index and various sub-indices were slightly higher than the manager’s prosperity index. It can be seen that under the special circumstances of the industry, merchants’ anti-risk capabilities and flexibility are slightly improved, and their dependence on the professional market has declined.

3. Predictive index

Data show that in terms of managers, the next manager’s prosperity index is 19.35, down 31.30 percentage points from 50.65 in December; the next operating environment index is 17.74, down 32.91 percentage points from 50.65 in December. In terms of merchants, the next merchants’ prosperity index is 39.58, down 11.41 percentage points from 50.99 in December; the next operating environment index is 37.85, down 12.86 percentage points from 50.71 in December. The four pre-judgment indexes have all fallen sharply. It can be seen that the operating environment in the next stage is uncertain. Managers and merchants are pessimistic about the operation of the next month. The impact of the COVID-19 on the market and business operations will continue for a period of time.

(contributed by CATA)

ALL COMMENTS